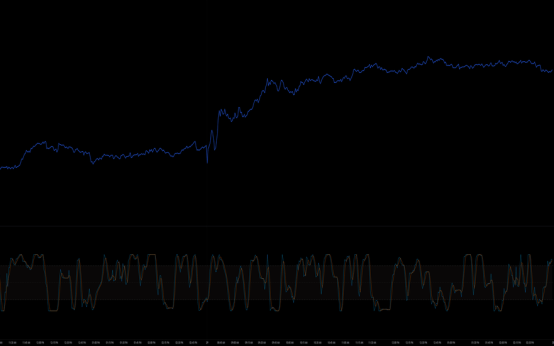

Kaufman Adaptive Moving Average Trending Up for Federal Signal Corp (FSS) News Kaufman Adaptive Moving Average Trending Up for Federal Signal Corp (FSS) 6 years ago admin 77

Checking on the Valuation For Shares of Zymeworks Inc. (TSX:ZYME), Talend S.A. (NasdaqGM:TLND) News 6 years ago Checking on the Valuation For Shares of Zymeworks Inc. (TSX:ZYME), Talend S.A. (NasdaqGM:TLND)

Consensus EPS Watch for Royal Caribbean Cruises Ltd. (NYSE:RCL) News 6 years ago Consensus EPS Watch for Royal Caribbean Cruises Ltd. (NYSE:RCL)

Estimates in Focus for Shares of Royal Caribbean Cruises Ltd. (NYSE:RCL) News 6 years ago Estimates in Focus for Shares of Royal Caribbean Cruises Ltd. (NYSE:RCL)

Caribbean Holdings International Corp (CBBI): Watching the Stochastic RSI on This Stock News 6 years ago Caribbean Holdings International Corp (CBBI): Watching the Stochastic RSI on This Stock

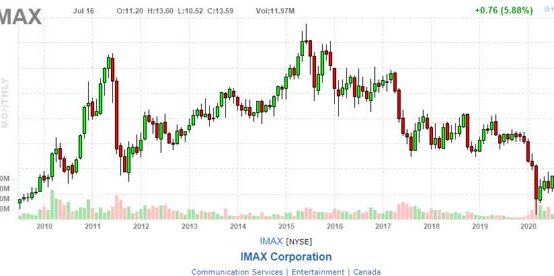

Signal Update on Shares of Imax Corp (IMAX): Weighted Alpha Hits -3.90 News 6 years ago Signal Update on Shares of Imax Corp (IMAX): Weighted Alpha Hits -3.90

Kaufman Adaptive Moving Average Trending Up for Federal Signal Corp (FSS) News admin 6 years ago 77 Kaufman Adaptive Moving Average Trending Up for Federal Signal Corp (FSS)

Checking on the Valuation For Shares of Zymeworks Inc. (TSX:ZYME), Talend S.A. (NasdaqGM:TLND) News admin 6 years ago 59 Checking on the Valuation For Shares of Zymeworks Inc. (TSX:ZYME), Talend S.A. (NasdaqGM:TLND)

Consensus EPS Watch for Royal Caribbean Cruises Ltd. (NYSE:RCL) News admin 6 years ago 53 Consensus EPS Watch for Royal Caribbean Cruises Ltd. (NYSE:RCL)

Estimates in Focus for Shares of Royal Caribbean Cruises Ltd. (NYSE:RCL) News admin 6 years ago 76 Estimates in Focus for Shares of Royal Caribbean Cruises Ltd. (NYSE:RCL)

Caribbean Holdings International Corp (CBBI): Watching the Stochastic RSI on This Stock News admin 6 years ago 56 Caribbean Holdings International Corp (CBBI): Watching the Stochastic RSI on This Stock

Signal Update on Shares of Imax Corp (IMAX): Weighted Alpha Hits -3.90 News admin 6 years ago 67 Signal Update on Shares of Imax Corp (IMAX): Weighted Alpha Hits -3.90

Can This Stock Rally? Weighted Alpha Reaches +9.00 For Perspecta Inc (PRSP) News admin 6 years ago 74 Can This Stock Rally? Weighted Alpha Reaches +9.00 For Perspecta Inc (PRSP)

North American Income Trust [The] Plc (NAIT.L) Technicals Take Center Stage News admin 6 years ago 50 North American Income Trust [The] Plc (NAIT.L) Technicals Take Center Stage

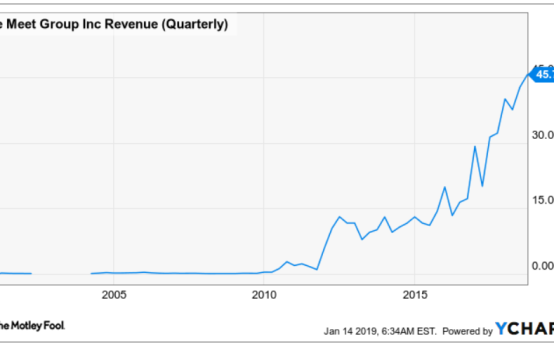

Fast Growing Stock in Focus: The Meet Group, Inc. (NASDAQ:MEET) News admin 6 years ago 34 Fast Growing Stock in Focus: The Meet Group, Inc. (NASDAQ:MEET)

Investors Peering into the Details on Computer Services, Inc. (OTCPK:CSVI) News admin 6 years ago 47 Investors Peering into the Details on Computer Services, Inc. (OTCPK:CSVI)

Checking on the Valuation For Shares of Zymeworks Inc. (TSX:ZYME), Talend S.A. (NasdaqGM:TLND)

Checking on the Valuation For Shares of Zymeworks Inc. (TSX:ZYME), Talend S.A. (NasdaqGM:TLND)  Consensus EPS Watch for Royal Caribbean Cruises Ltd. (NYSE:RCL)

Consensus EPS Watch for Royal Caribbean Cruises Ltd. (NYSE:RCL)  Estimates in Focus for Shares of Royal Caribbean Cruises Ltd. (NYSE:RCL)

Estimates in Focus for Shares of Royal Caribbean Cruises Ltd. (NYSE:RCL)  Caribbean Holdings International Corp (CBBI): Watching the Stochastic RSI on This Stock

Caribbean Holdings International Corp (CBBI): Watching the Stochastic RSI on This Stock  Signal Update on Shares of Imax Corp (IMAX): Weighted Alpha Hits -3.90

Signal Update on Shares of Imax Corp (IMAX): Weighted Alpha Hits -3.90  Kaufman Adaptive Moving Average Trending Up for Federal Signal Corp (FSS)

Kaufman Adaptive Moving Average Trending Up for Federal Signal Corp (FSS)  Can This Stock Rally? Weighted Alpha Reaches +9.00 For Perspecta Inc (PRSP)

Can This Stock Rally? Weighted Alpha Reaches +9.00 For Perspecta Inc (PRSP)  North American Income Trust [The] Plc (NAIT.L) Technicals Take Center Stage

North American Income Trust [The] Plc (NAIT.L) Technicals Take Center Stage  Fast Growing Stock in Focus: The Meet Group, Inc. (NASDAQ:MEET)

Fast Growing Stock in Focus: The Meet Group, Inc. (NASDAQ:MEET)  Investors Peering into the Details on Computer Services, Inc. (OTCPK:CSVI)

Investors Peering into the Details on Computer Services, Inc. (OTCPK:CSVI)