The MF Rank (Magic Formula Rank) is a formula that helps identify a valuable company trading at a good price. The formula is calculated by looking at companies that have a high earnings yield as well as a high return on invested capital. The MF Rank of DCC plc (DCC.L) is 2705. A company with a low rank is considered a good firm to invest in. The Magic Formula was introduced in a book written by Joel Greenblatt, entitled, “The Little Book that Beats the Market”. A favorite book amongst Wall Street’s elite.

Equity market investing has a way of provoking strong emotions. When markets become frantic, investors may feel compelled to make decisions that they might not normally make. Having the proper perspective and staying focused can help the individual investor stay committed to the previously created plan. Trying to predict the day to day movements of the stock market can be extremely difficult. Even the top professionals may get thrown for a loop every now and then. Chasing winners and holding onto losers may be a recipe for portfolio disaster over the long run. Investors who are able to stay calm and think logically should be able to better position themselves when markets become stormy.

Benjamin Graham, professor and creator of value investing principles, was one of the first investors to consistently screen the market looking for bargain companies based on value factors. He didn’t have databases such as ValueSignals at his disposal, but used people like his apprentice Warren Buffet to fill out stock sheets with the most important data.

Graham was always on the watch for firms that were so discounted, that if the company went into liquidation, the proceeds of the assets would still return a profit.

The ratio he used to identify these companies was Net Current Asset Value or NCAV. This ratio is much more stringent compared to book value (total assets – total liabilities) and is calculated as follows:

NCAV = Current Assets – Total LiabilitiesCurrent Assets = Cash & ST Investments + Inventories + Accounts Receivable

Graham was only happy if he could buy the company at 2/3 of the NCAV. That’s the sort of margin of safety he was looking for.

This strategy was very successful during the years after Graham published it in his book ‘Security analysis’ in 1934 and also in more recent studies it has proven to provide superior results. A study done by the State University of New York to prove the effectiveness of this strategy showed that from the period of 1970 to 1983 an investor could have earned an average return of 29.4%, by purchasing stocks that fulfilled Graham’s requirement and holding them for one year. Nowadays it’s very difficult to find companies that meet Graham’s criteria.

NCAV to Market are calculated as follows:

NCAV-to-Market Ratio = NCAV divided by Market Cap

DCC plc (DCC.L) has an NCAV to Market value of -0.228785.

Value Composite Three (VC3) is another adaptation of O’Shaughnessy’s value composite but here he combines the factors used in VC1 with buyback yield. This factor is interesting for investors who’re looking for stocks with the best value characteristics, but are indifferent to whether these companies pay a dividend.

VC3 is the combination of the following factors:

Price-to-BookPrice-to-EarningsPrice-to-SalesEBITDA/EVPrice-to-Cash flow

Buyback Yield

As with the VC1 and VC2, companies are put into groups from 1 to 100 for each ratio and the individual scores are summed up. This total score is then put into groups again from 1 to 100. 1 is cheap, 100 is expensive.

The scorecard also displays variants of the VC3 where the score is calculated for the selected company compared to peer companies in the same industry, industry group or sector.

Please note that we use Book-to-Market instead of P/B since it allows a more accurate sorting compared to P/B. Stocks with a high B/M show up at the top of the list, stocks with negative B/M are at the bottom of the list. For the same reason we use Earnings-to-Price instead of Price-to-Earnings and Cash flow-to-price instead instead of Price-to-cash flow.

Also important is that we always make sure that companies with the same score get added to the same percentile. For stock universes where the number of stocks is less than 100, we make sure that the stocks are still allocated to percentiles from 0 to 100 instead of 0 to the total number of stocks. This is particularly relevant for the industry, industry group or sector variants where if additional filters are used, the number of stocks often drops below 100.

DCC plc (DCC.L) has a VC3 of 28.

Gross Profitability

DCC plc (DCC.L) has Gross Profitability of 0.230702

Robert Novy-Marx, a professor at the university of Rochester, discovered that gross profitability – a quality factor – has as much power predicting stock returns as traditional value metrics. He found that while other quality measures had some predictive power, especially on small caps and in conjunction with value measures, gross profitability generates significant excess returns as a stand alone strategy, especially on large cap stocks.

Gross Profitability is calculated as follows:

Gross Profitability = (Net Sales or Revenues−Cost of Goods Sold)/Total Assets

Novy-Marx’s key insight was that you don’t need to go further down the income statement as these numbers may get manipulated with accounting tricks. To identify really profitable firms, one should look at the top line, not the bottom line.

In one of his papers, Novy-Marx compares gross profitability to the other most famous strategies such as Greenblatt magic formula, Piortoski F-Score, etc.

ERP5 Rank

The ERP5 Rank is an investment tool that analysts use to discover undervalued companies. The ERP5 looks at the Price to Book ratio, Earnings Yield, ROIC and 5 year average ROIC. The ERP5 of DCC plc (DCC.L) is 3179. The lower the ERP5 rank, the more undervalued a company is thought to be.

FCF Yield 5yr Avg

The FCF Yield 5yr Average is calculated by taking the five year average free cash flow of a company, and dividing it by the current enterprise value. Enterprise Value is calculated by taking the market capitalization plus debt, minority interest and preferred shares, minus total cash and cash equivalents. The average FCF of a company is determined by looking at the cash generated by operations of the company. The Free Cash Flow Yield 5 Year Average of DCC plc (DCC.L) is 0.023594. The FCF Yield currently stands at 0.03302.

Stock analysis typically falls into two main categories. Some investors may prefer technical analysis, and others may prefer to study the fundamentals. Many investors will keep an eye on both. Technical analysis involves trying to project future stock price movements based on prior stock activity. Technicians strive to identify chart patterns and study other historical price and volume data. Technical investors look to identify trends when assessing a stock. The trend is typically considered to be the main direction of the share price. Trends are generally categorized as either up, down, or sideways. If a bullish trend is spotted, the trader may expect the upward trend to continue and thus try to capitalize on further upward action.

Kaufman Adaptive Moving Average Trending Up for Federal Signal Corp (FSS)

Kaufman Adaptive Moving Average Trending Up for Federal Signal Corp (FSS)  Checking on the Valuation For Shares of Zymeworks Inc. (TSX:ZYME), Talend S.A. (NasdaqGM:TLND)

Checking on the Valuation For Shares of Zymeworks Inc. (TSX:ZYME), Talend S.A. (NasdaqGM:TLND)  Consensus EPS Watch for Royal Caribbean Cruises Ltd. (NYSE:RCL)

Consensus EPS Watch for Royal Caribbean Cruises Ltd. (NYSE:RCL)  Estimates in Focus for Shares of Royal Caribbean Cruises Ltd. (NYSE:RCL)

Estimates in Focus for Shares of Royal Caribbean Cruises Ltd. (NYSE:RCL)  Caribbean Holdings International Corp (CBBI): Watching the Stochastic RSI on This Stock

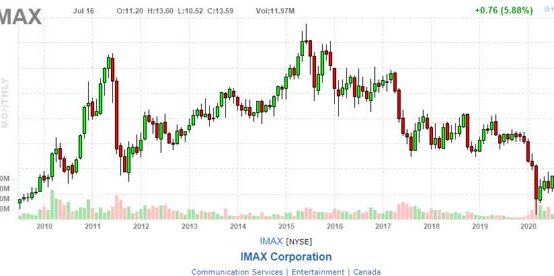

Caribbean Holdings International Corp (CBBI): Watching the Stochastic RSI on This Stock  Signal Update on Shares of Imax Corp (IMAX): Weighted Alpha Hits -3.90

Signal Update on Shares of Imax Corp (IMAX): Weighted Alpha Hits -3.90